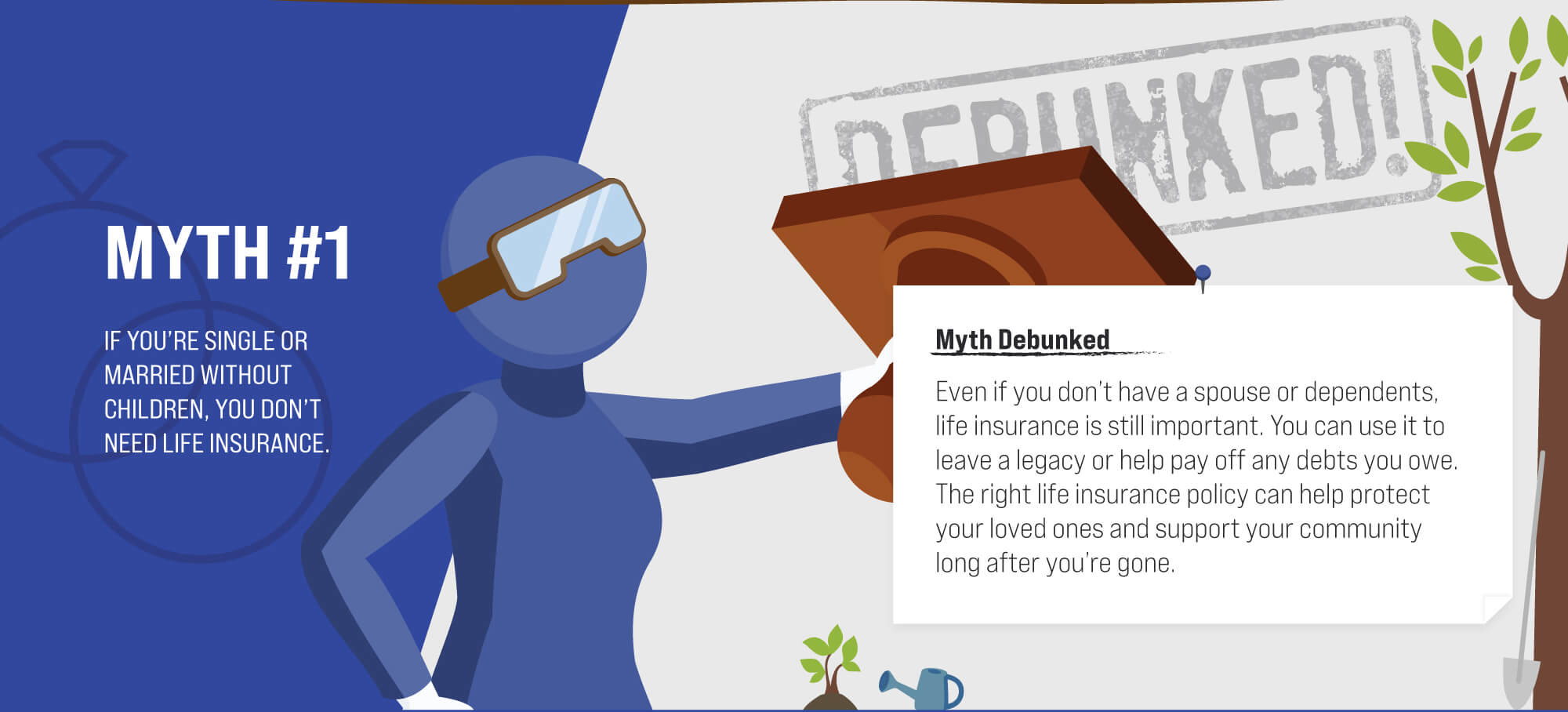

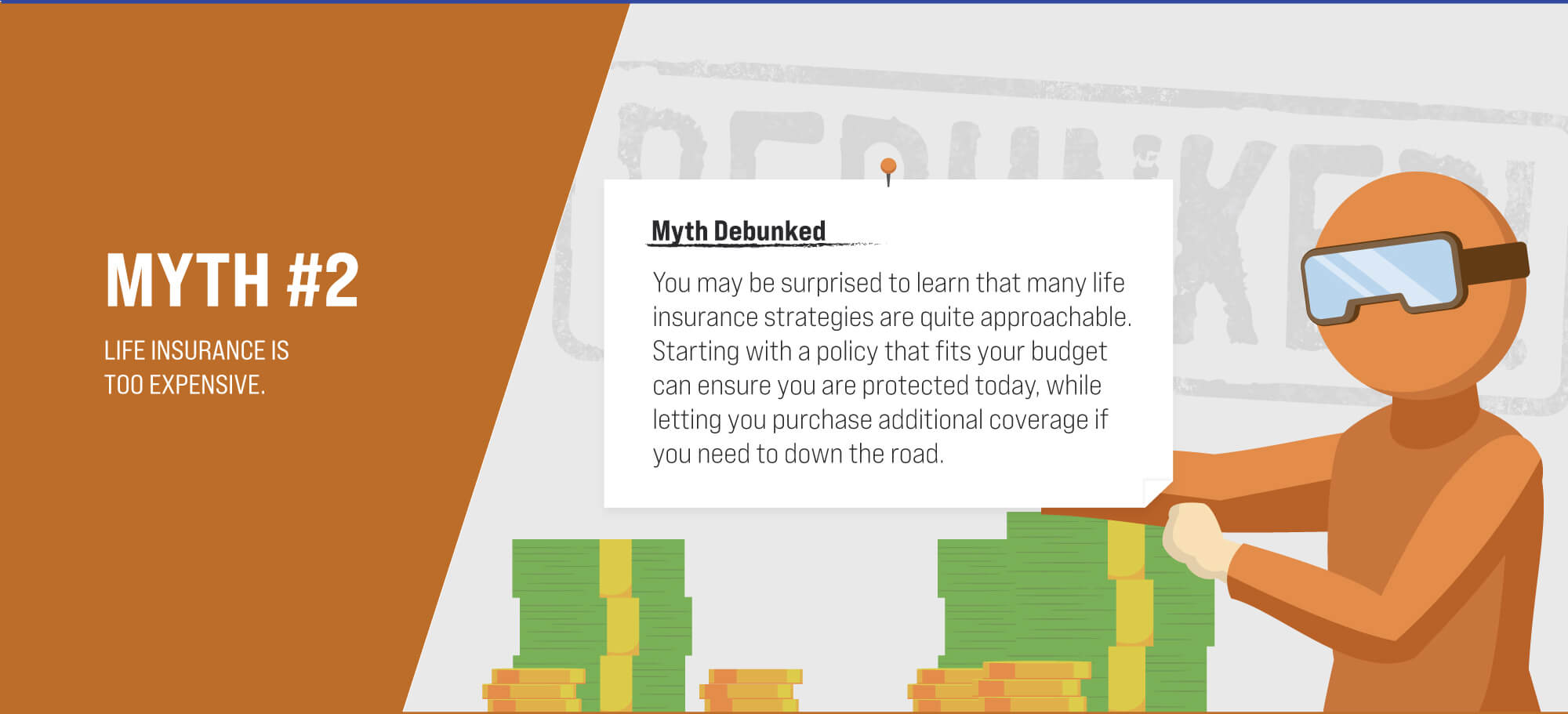

Life Insurance Myths: Debunked

Beware of these traps that could upend your retirement.

Learning more about gold and its history may help you decide whether it has a place in your portfolio.

Estate strategies for millennials may sound like less of a concern than retirement, but young adults should prepare now.